➺ Recent work | Home

Project summary

Grant mortgage customers a further valuation

Nationwide

I integrated a complex further valuations process into Nationwide's mortgage application journey. I interviewed mortgage and property hub teams to align with business objectives, mapped the customer journey, conducted research, tested prototypes, and presented findings.

The challenge

Further valuations is the process by which a customer can have their home revalued so that they may take a further advance which they may use for purchases like home improvements.

Adding further valuations to the remortgage journey could prevent an estimated 25% remortgage journeys being finished with offline assistance.

Understand the business objectives

I first needed to get an understanding of the further advance journey from the perspective of the business. I conducted interviews with the mortgage team and the team at the property hub. They were tasked with making the decisions over whether to agree to a further valuation.

Conduct generative research

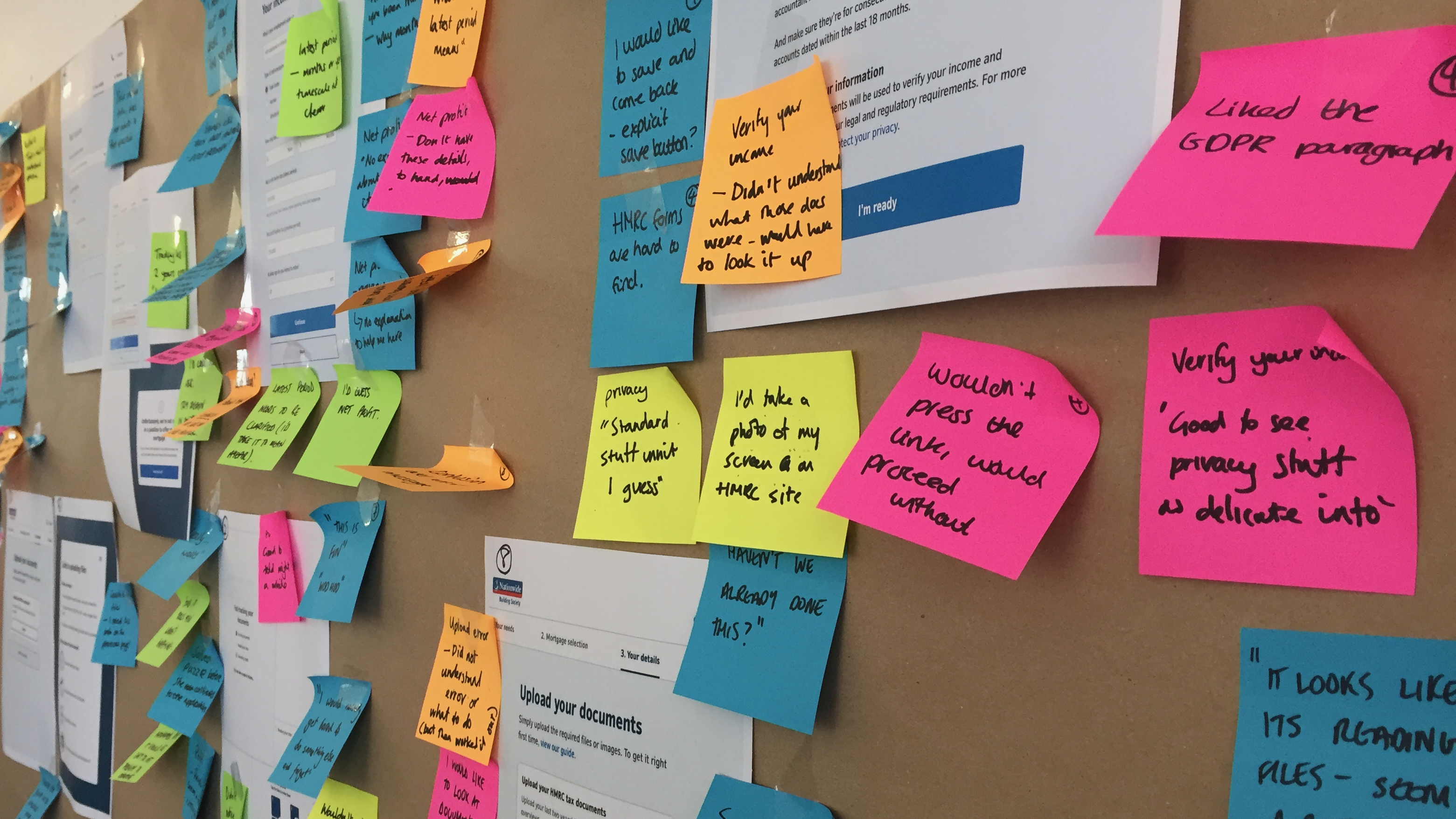

Once I understood the business requirements I began research to understand customers feelings around a property valuation during a remortgage application by creating a prototype and testing with users.

Create a prototype

Based on the insights from user research and knowledge gained about the business requirements I created a prototype to meet the needs of users. I created a hypothesis to be the basis of a prototype created in InVision. I wrote the recruitment brief and discussion guide for the researcher to follow during the testing process.

The research consisted of one-to-one interviews with five participants in a lab setting, asking for feedback and reactions related to the digital prototype tested on a mobile device.

Create a customer journey map

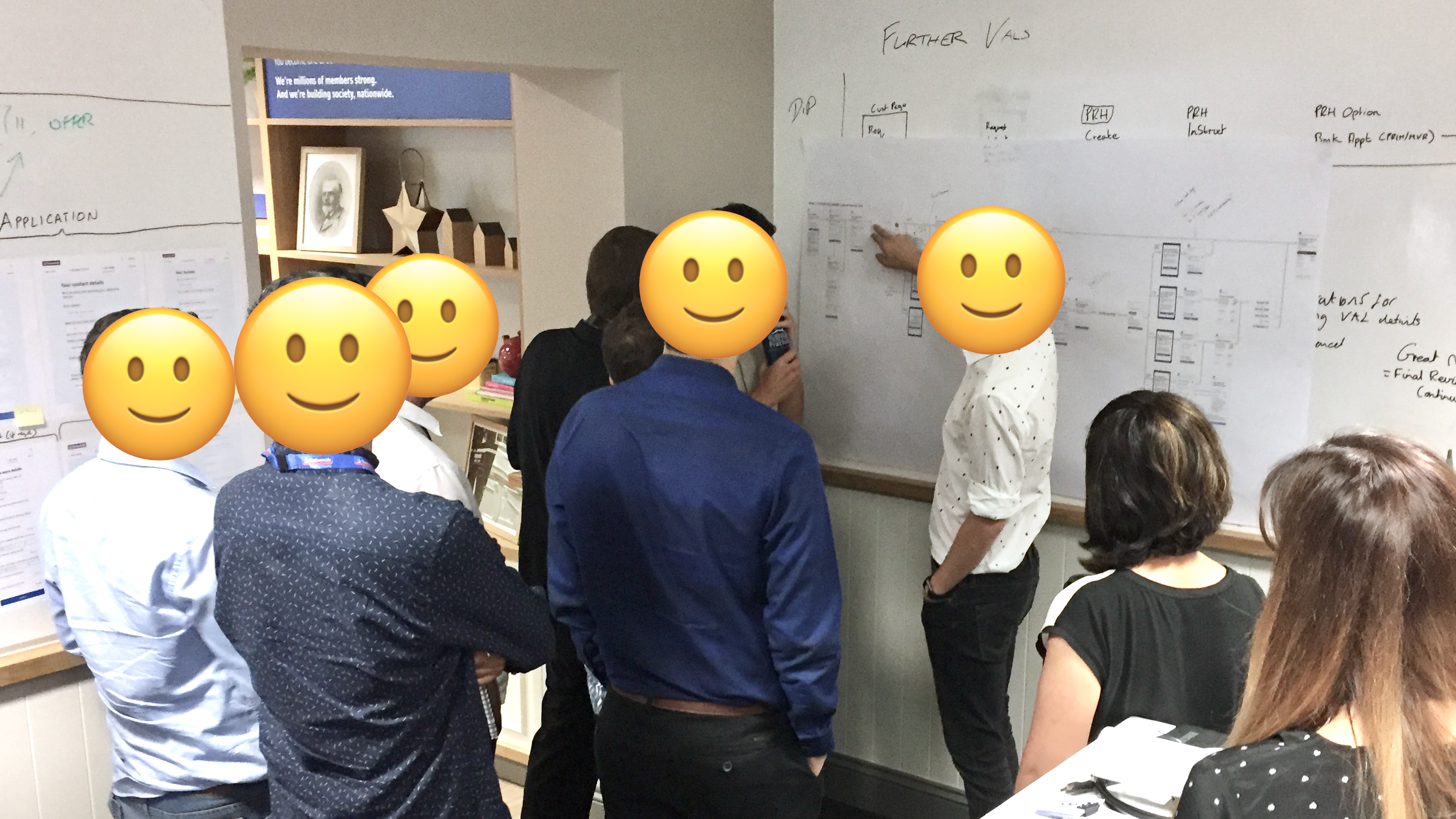

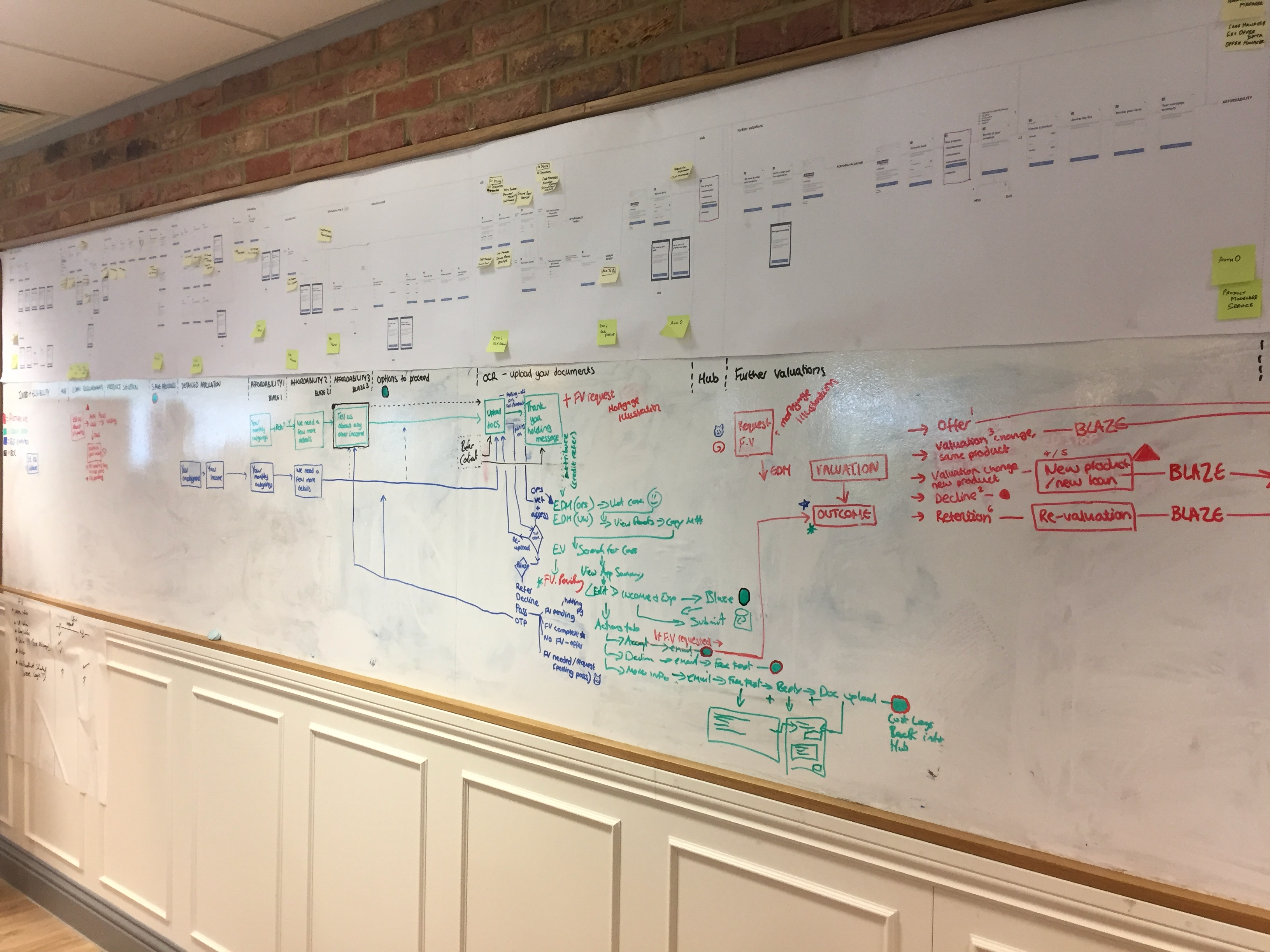

To further ensure all scenarios were accounted for, and to aid communication within the team, I created a customer journey map.

I also created a full customer journey map to show how further valuations fit in with the whole remortgage journey

I printed the whole journey and stuck it to the wall. This proved invaluable to the project team of developers and leaders who added notes and used it as a centre of discussion when dealing with issues and proposing solutions.

The developers used it as an anchor to design and help visualise the backend requirements

The observations uncovered insights into why customers hesitate when requesting a further advance. I was able to make recommendations to ensure customers were informed of the process and increase the likelihood of getting to offer. At the same time fulfilling the business requirements of reducing dropouts, the research revealed a lack of understanding of the complex mortgage terminology and process (such as ‘LTV’ and reasons for valuation) which I communicated to the research teams.

I presented the findings back to the team in the weekly show and tell. I also included a video showcasing the key observations. This helped with understanding the issues and delivered greater impact when communicating the research to the wider business.

The recommendations were implemented into the customer journey. I tested the user journey again with users under similar conditions. This proved the hypothesis, allowed me to refine the content and gave the team confidence to deliver the journey.

✻